Deciding which mortgage loan option would be best for you is a complex process. If you’re looking to choose between a 15-year fixed rate mortgage and a 30-year fixed rate mortgage you must evaluate all the different factors to ensure that you’re making a home loan decision that you’re comfortable with. Find out the differences of a 15-year fixed mortgage vs. a 30-year fixed mortgage, compare pros and cons, and decide which one would be better for you.

What’s a 30-Year Fixed Mortgage

With a 30-year mortgage, you’re paying principal and interest every month over the span of 30 years. As a result, mortgage payments will be smaller. With a 30-year fixed mortgage, it’ll take longer to pay off. This is because you’re borrowing the same amount of money but paying it back over a longer period of time compared to a 15-year fixed mortgage. Another essential point to note is that 30-year fixed mortgages have higher interest rates since they’re spread out over a longer period and have more time to accrue.

What’s a 15-Year Fixed Mortgage

A 15-year fixed mortgage is when you pay both principal and interest over a period of 15 years. The monthly payments are higher compared to the 30-year mortgage. But you’ll pay off the balance faster since it’s a 15-year term. Interest payments are lower on a 15-year fixed mortgage since the interest has less time to accumulate. Interest rates are also historically lower on a 15-year mortgage vs. 30-year.

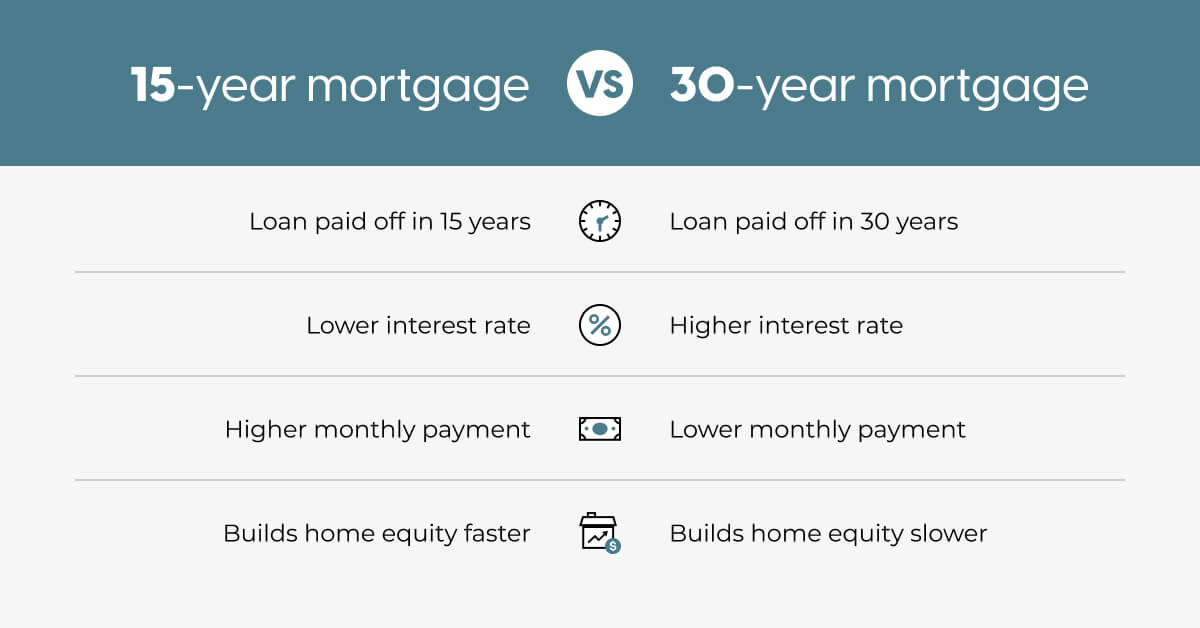

Differences Between a 15-Year vs. 30-Year Mortgage

Is the only difference between the two types of mortgages the length of time you have to pay it off? Well, not exactly.

Depending whether you choose a 15-year mortgage or a 30-year mortgage, there will be a domino effect on other aspects, such as the interest over the life of the loan, the total monthly payment, and the total number of mortgage payments. This chart shows you a side-by-side comparison with the differences between a 15-year and 30-year fixed mortgage:

| 15-Year Fixed Mortgage | 30-Year Fixed Mortgage |

|---|---|

| Loan paid off in 15 years | Loan paid off in 30 years |

| Lower interest rate | Higher interest rate |

| Higher monthly payment | Lower monthly payment |

| Builds home equity faster | Builds home equity slower |

Some of the key differences to note between a 15-year vs. 30-year mortgage include:

Length of the Mortgage Loan

The first difference, of course, is the amount of time you have to pay off the loan. There are pros and cons of choosing a 15-year vs. 30-year mortgage based on the monthly payments you’re responsible for. If you choose the 30-year term, your monthly mortgage payment will be considerably lower.

A 30-year fixed-rate mortgage could be a suitable option if you’re looking for more flexibility with payments or just want some breathing room depending on personal finances.

But compared to the 15-year fixed mortgage, you’ll be making monthly payments for a far longer time than a 15-year fixed-rate mortgage. While the monthly payments for the 15-year term are higher, you’re paying off the loan considerably faster and that much closer to owning your home.

Interest Rate

Interest rates should always be a consideration when thinking about monthly mortgage payments and whether a 15-year vs. 30-year mortgage is right for you. With a 30-year fixed-rate mortgage, you have smaller monthly payments overall.

However, the interest rate is higher. That means you’re paying more on interest over the life of the loan rather than the principal amount, even if the monthly payment itself is a smaller amount.

You could potentially offset this by making extra payments where possible to reduce the total amount you have to pay, but that’s not always an option for everyone.

When it comes to evaluating the principal and the interest for the two types of mortgages, the interest rate is lower when buying a home with a 15-year fixed-rate mortgage. So while the monthly payments are higher, you pay less interest over time.

Since the interest rate is lower for a 15-year vs. 30-year mortgage, that’s often the deciding factor for which option to go. For a 15-year fixed-term mortgage, the interest has less time to accrue, and it saves homeowners more money in the long term.

Monthly Payments

Another key difference is the monthly mortgage payment itself. The trade-off between 15 years and 30 years is how you balance short-term and long-term financial goals based on your current circumstances.

For example, if you opt for the 30-year fixed mortgage, you’ll have smaller monthly payments, but you’re making payments for a longer time and paying more interest. However, because it’s distributed over 30 years, it may not feel like that much of a difference in the end. But with the 15-year fixed-rate mortgage, you’re paying a lot more in the short-term, but then you’re saving on interest over the life of the loan in the long term.

Ultimately, choosing what kind of monthly payment to go for when deciding on mortgages is very much a personal decision based on personal finances. Consider other payments such as property taxes and closing costs that must be made during the time of purchase.

Additionally, you’ll need to consider other monthly payments you may have, such as credit cards, cars, and insurance, that may impact how much you’re willing to pay on your home loan and what you can reasonably afford monthly. Calculate that against interest payments and interest rates that you’re currently finding on 15-year vs. 30-year mortgage options to identify what would be best for your specific circumstances.

Should you do a 15-year or a 30-year mortgage?

Running the numbers can help you identify what you’re most comfortable with paying in the short-term or long-term when buying a home and enable you to feel more confident during the homebuying process.

Using a mortgage calculator and running different scenarios between the two types of mortgage terms can help with deciding how much of a down payment to put down and what estimated monthly mortgage payments you can expect. CrossCountry Mortgage has a variety of resources to help you become a homeowner, including a mortgage calculator to compare two mortgage loans and identify what’s best for you.

If you have more questions, contact one of our loan officers.

.jpg.aspx)